After analyzing MERESE and biodiversity credits, a new figure emerges that combines regulation, territorial planning, and market logic: habitat banks.

Let us briefly recall the difference:

• MERESE is an scheme through which those who benefit from an ecosystem service — such as water provisioning — finance conservation or restoration actions. Their logic is retributive: payment is made to maintain or improve a service.

• Biodiversity credits, by contrast, represent verifiable ecological improvements that can be voluntarily acquired by companies or individuals to meet sustainability commitments or generate a net biodiversity gain.

What is a habitat bank?

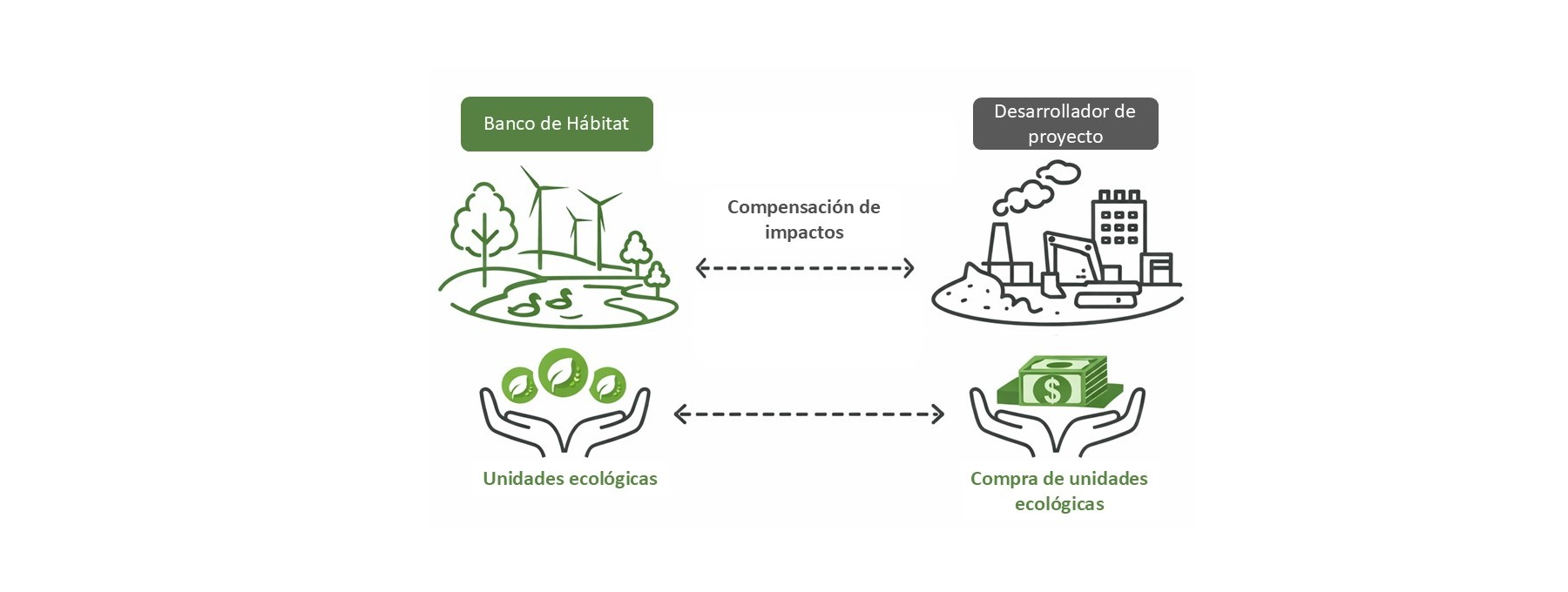

A habitat bank is a regulated environmental offset mechanism through which an operator restores, conserves, or enhances an ecosystem in advance, generating verified and ecologically equivalent units that can be acquired by projects to compensate residual impacts authorized by the environmental authority.

These units may only be released once verifiable ecological performance milestones have been met and are backed by long-term management and permanence commitments.

Its logic is clear:

• Restoration occurs before the impact.

• Ecologically equivalent units are generated.

• Long-term management and monitoring are guaranteed.

• Credits are used by buyers to comply with regulatory obligations.

Consequently:

• It is not a fund.

• It is not an isolated project.

• It is a planned and professionally managed ecological infrastructure.

An additional instrument within the conservation portfolio

In Peru, habitat banks do not replace existing instruments. Rather, they complement a territorial conservation portfolio that already includes:

• Protected natural areas (ANP): areas under state administration or management contracts that seek financing to close management gaps. In Peru, these are managed by SERNANP.

• Conservation concessions: mechanisms that protect specific forest areas through long-term contracts, often compatible with voluntary schemes. In Peru, concessions are granted by SERFOR.

• Private reserves and community territories, such as Private Conservation Areas (ACP) recognized by the Ministry of the Environment, which can implement preservation actions and potentially generate tradable units.

Note: In a forthcoming post, we will further develop the legal framework for habitat banks in Peru.

Can habitat banks emerge from these categories?

There is a strong argument that a habitat bank does not necessarily require the creation of a new territorial category. It could be structured on existing figures — such as ACPs, ACRs, or concessions — provided that:

• A clear baseline is established.

• Ecological equivalence metrics are defined.

• Permanence and monitoring are guaranteed.

• Double counting is avoided.

• Real additionality is demonstrated relative to the existing regulatory baseline.

In this sense, a habitat bank could become an additional layer of management and financing over territories already legally recognized for conservation, transforming them into structured issuers of biodiversity units.

However, without clear rules, there is a risk of turning already protected areas into financial instruments without generating additional ecological improvement.

The difference ultimately lies in the operational and accounting framework under which ecological results are managed.

References

UNDP. 2010. Habitat Banking in Latin America and Caribbean: A Feasibility Assessment.